One of the most well-known concepts of economics and business is market equilibrium. It’s where supply and demand in the marketplace meet so that prices remain stable. Whether an economics student is pondering basic theories, a business person devising an approach to a market or an expert is trying to figure out developments, disparities comprehended will be vital to decoding the market and wrapping up choices.

In this blog, we will see the definition of market equilibrium, how supply and demand interact to achieve equilibrium, the factors affecting equilibrium, real-life examples of how it works, and its current relevance in modern markets. You will also understand how this principle affects real life and how it is applied in policy.

What is Market Equilibrium?

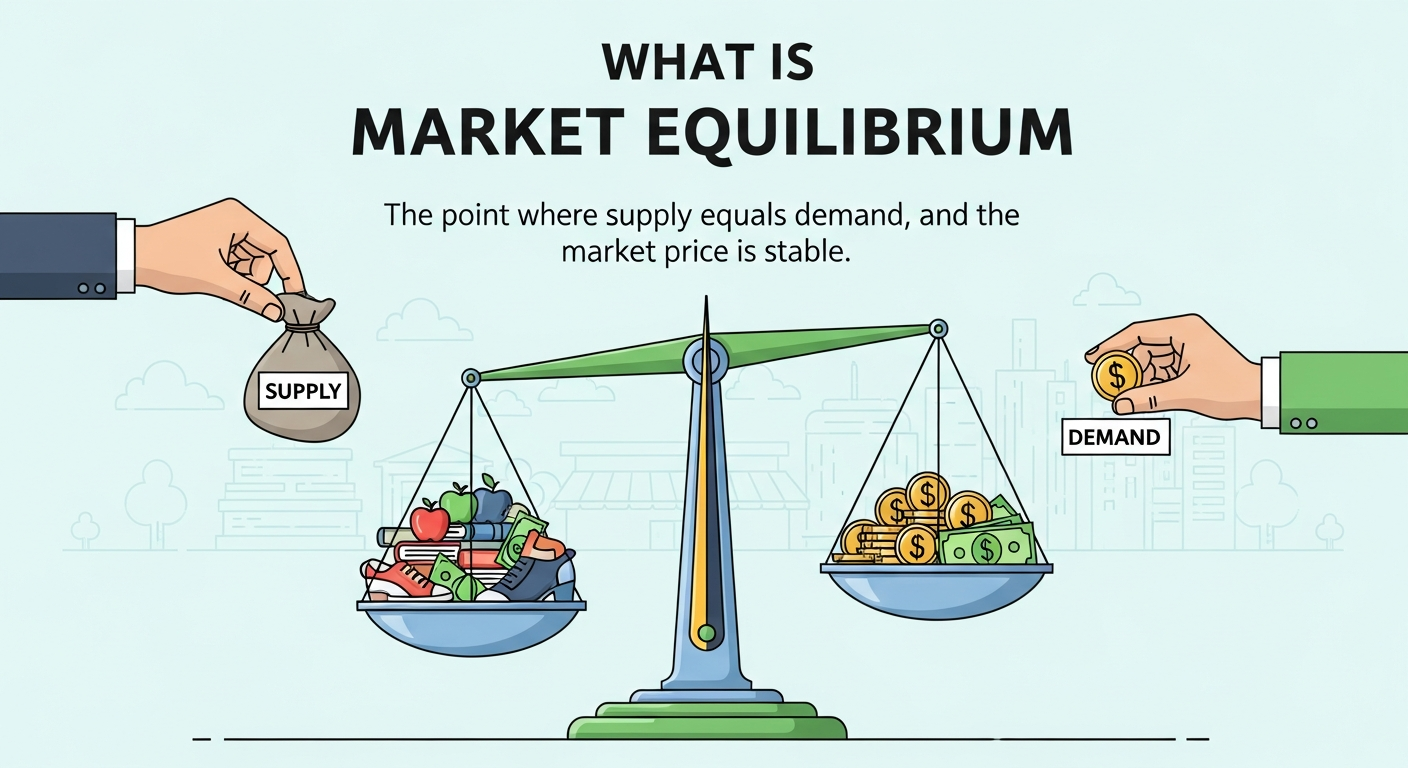

Market equilibrium is when the amount of goods or services producers are willing to offer to consumers at a certain price equals the amount consumers are willing to purchase at that same price. This equilibrium refuses to create either a deficit or excess in the market, typically curbing prices.

At this time, the price in the marketplace is known as the “equilibrium price,” and the portion of goods traded is the “equilibrium quantity.” This balance can be maintained if circumstances in the market stay unchanged. In reality, however, markets are not static and they constantly undergo changes in terms of demand, supply, and other external factors that are bound to shift the market out of equilibrium.

Take the movie ticket market in a small town, for example. High ticket prices might result in half–filled theaters in cinemas, as consumers will be reluctant to pay for them due to a lack of demand. If tickets are too inexpensive, theaters may be packed, but they won’t generate enough revenue to cover production costs. At equilibrium, ticket prices are good so that the number of people willing to pay the asking price matches the number of seats available.

To explore this concept further, read Investopedia’s guide on Market Equilibrium.

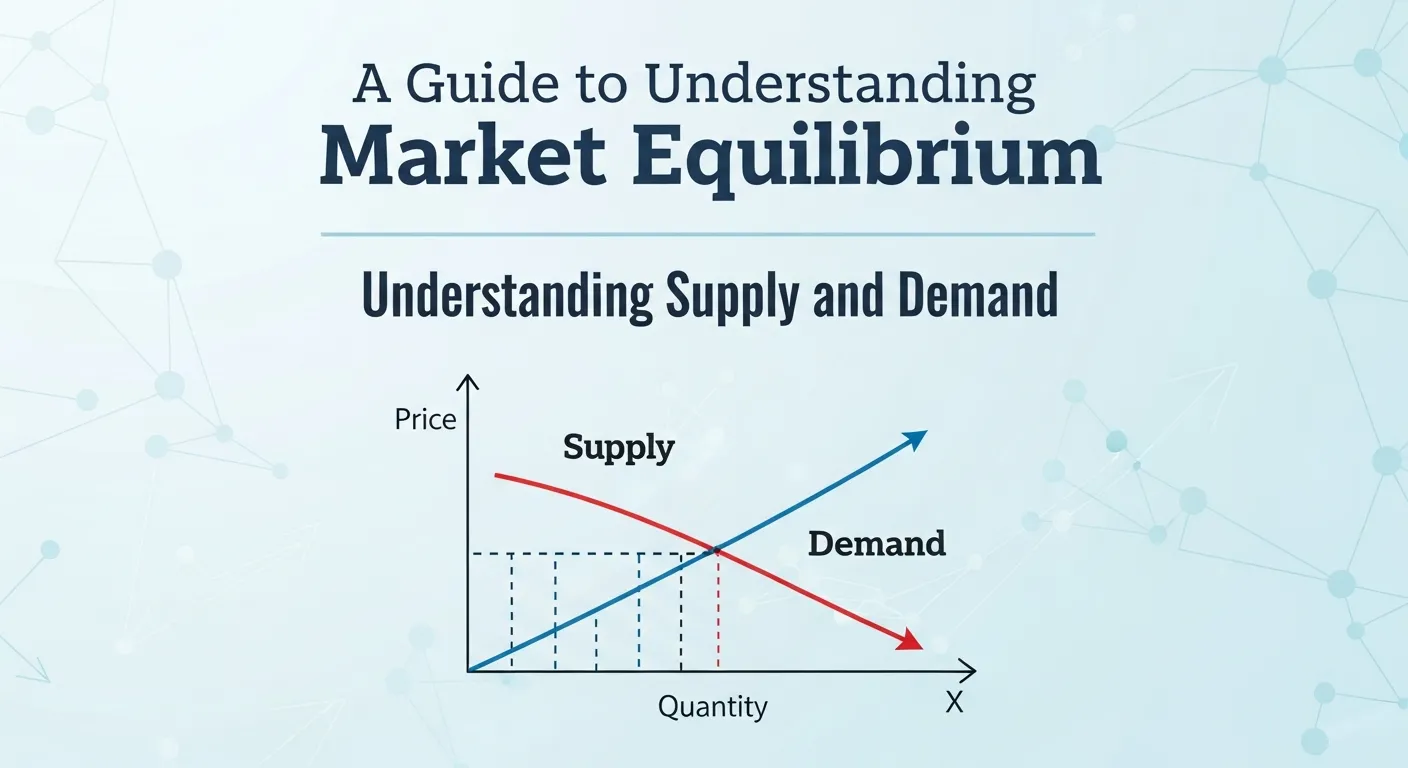

Understanding Supply and Demand

Market equilibrium hinges on two significant economic forces: supply and demand.

What is Demand?

Demand is the amount of a good or service that a consumer is willing and able to buy across a range of prices. With lower prices, the demand is higher, while higher prices reduce demand. This relationship can be represented with the “demand curve,” sloping downwards from left to right.

For example, if a shop begins to sell coffee at $1 per cup, then it will be popular among customers. But if the price rises to $5 a cup, fewer people will feel it is worth paying the cost and, therefore, the demand will fall.

What is Supply?

Supply is the amount of goods or services that producers are willing and able to sell at different price points. The opposite is true for supply: The supply curve slopes up because higher prices incentivize producers to produce more of a good.

Taking the example of coffee, if a café is able to sell coffee at $5 a cup, it’s probably going to make a higher profit and thus will want to sell as much as possible. But when consumers are only paying $1 a cup, there’s less motivation to make enormous amounts of it.

The Interaction of Supply and Demand

The market reaches equilibrium when the supply curve intersects the demand curve. At this point:

- The equilibrium price ensures consumers buy exactly what producers can supply.

- Neither a surplus (too much supply) nor a shortage (too little supply) exists.

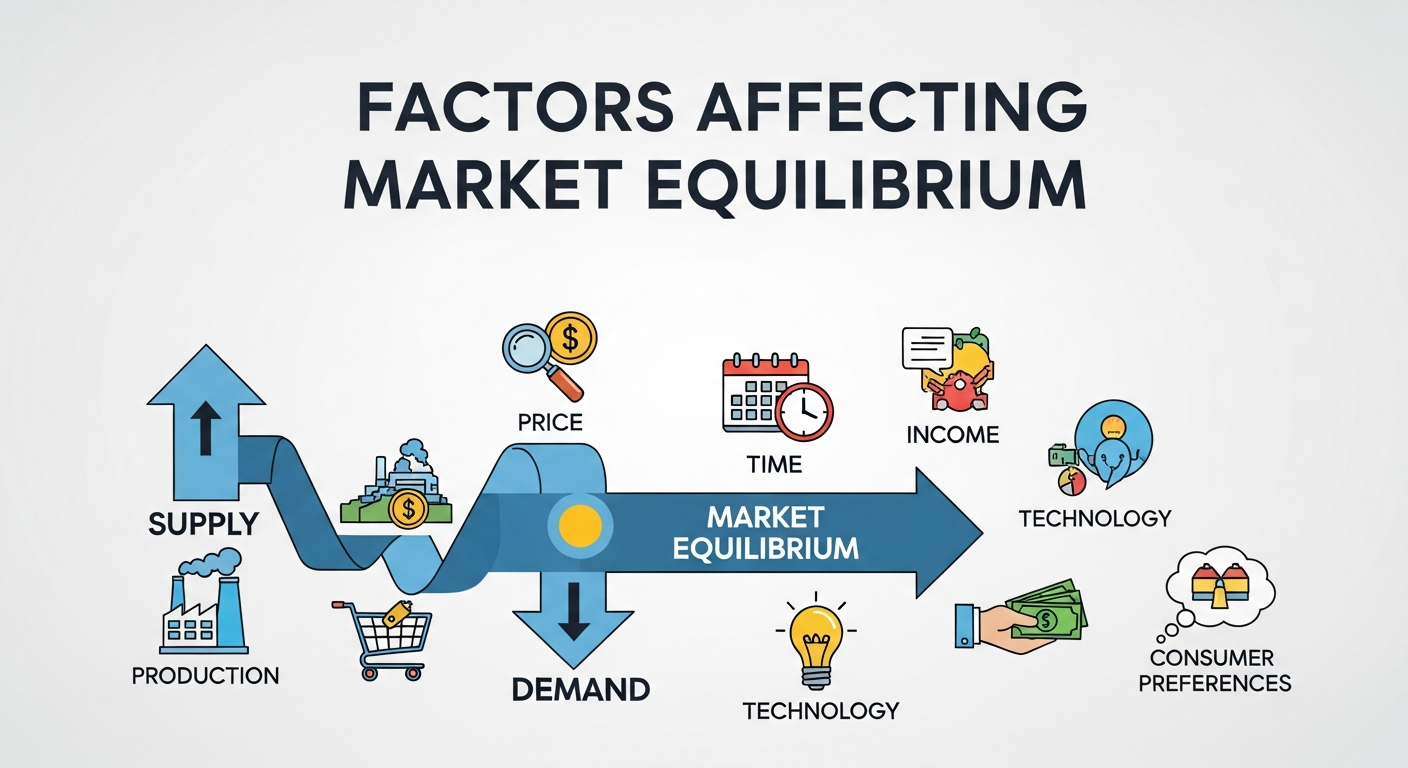

Factors Affecting Market Equilibrium

Markets are rarely static, as various factors influence both supply and demand. These shifts affect equilibrium prices and quantities. Here are the primary factors:

Supply-Side Factors

- Production Costs: Changes in the cost of labor, raw materials, or technology can influence producers’ willingness to supply goods.

- Technological Advancements: Innovation can lower production costs, resulting in increased supply.

- Number of Sellers: More suppliers entering the market increases supply, moving equilibrium levels downward.

Demand-Side Factors

- Consumer Income: Increased income generally raises demand for goods, while a drop in income decreases it.

- Tastes and Preferences: Trends or societal shifts can dramatically alter demand (e.g., growing preference for electric cars).

- Price of Related Goods: The cost of complementary or substitute goods plays a role. For example, if gas prices drop, demand for fuel-efficient cars may decrease.

External Shocks

Economic recessions, global pandemics, and geopolitical events can disrupt supply and demand, pushing the market away from equilibrium temporarily.

These factors work like levers, causing supply and demand curves to shift up, down, left, or right, ultimately impacting equilibrium.

How is Market Equilibrium Determined?

Market equilibrium is mathematically determined by comparing supply and demand equations. Here’s an example:

- Demand Equation: Qd = 50 – 5P

(Qd represents quantity demanded, P represents price.)

- Supply Equation: Qs = 10 + 5P

(Qs represents quantity supplied.)

Finding equilibrium involves solving for P (price) when Qs = Qd.

- 50 – 5P = 10 + 5P

- Rearranging gives 40 = 10P

- Solving for P gives P = 4.

At a price of $4, the quantity demanded equals the quantity supplied, achieving market equilibrium.

These shifts in supply and demand play a vital role in every Product Market, influencing pricing and consumer behavior.

By utilizing such calculations, businesses and analysts can predict pricing and set inventory goals effectively.

Examples of Market Equilibrium

Example 1: Housing Market

In the housing market, equilibrium is visible when property prices reflect the balance between supply and demand. When demand for new homes increases, developers often respond by launching new housing projects. The same principle applies in business — understanding when and how to introduce offerings can determine success. If you’d like to learn more about the process, read this detailed guide on how to bring a product to market in 9 steps.

Example 2: Ride-Sharing Services

Platforms like Uber use algorithms to balance driver availability with rider demand. When demand surges (e.g., during rush hour), ride prices rise, incentivizing more drivers to join the platform. Prices stabilize once equilibrium is achieved.

These examples showcase how equilibrium isn’t just an academic concept, but a reality in markets we encounter daily.

Real-World Applications of Market Equilibrium

Understanding market equilibrium isn’t just for theorists; it has practical implications for businesses, policymakers, and consumers.

For Businesses

- Pricing Strategy: Equilibrium pricing ensures businesses maximize revenue without reducing demand — a key responsibility for a Product Marketing Manager.

- Inventory Management: Understanding shifts in equilibrium can help businesses prepare for changes in consumer purchasing patterns.

For Governments and Policymakers

- Setting Minimum Wage: Governments need to consider equilibrium in the labor market to prevent unemployment (caused by wage floors being set too high) or exploitation (caused by low wages).

- Price Controls: Policymakers may intervene to address price ceilings (e.g., rent control) or price floors (e.g., farm subsidies).

For Consumers

- Economic Awareness: Consumers inadvertently play a role in maintaining equilibrium. Being aware of factors influencing market prices empowers them to make informed purchasing decisions.

Market equilibrium touches most aspects of economic activity, making it a concept everyone, regardless of profession, should understand.

How Market Equilibrium Shapes the Modern Market Economy

In a market economy, prices act as signals that balance supply and demand. Market equilibrium ensures that these prices reflect both consumer preferences and production capabilities. When equilibrium is achieved, resources are used efficiently, benefiting producers, consumers, and society as a whole.

However, real-world markets—like the housing market or energy sector—rarely stay in perfect balance for long. Factors such as global trade, inflation, and consumer trends continuously influence price shifts and output levels. Understanding how equilibrium operates helps economists and policymakers maintain economic stability and forecast future changes.

Key Roles of Market Equilibrium in a Market Economy

-

Price Stability: Keeps prices predictable, helping both consumers and producers plan better.

-

Efficient Resource Allocation: Ensures goods and services are distributed based on real market demand.

-

Economic Forecasting: Helps analysts and governments identify growth or recession signals early.

-

Consumer Confidence: Stable markets encourage consumer spending and long-term investment.

-

Reduced Waste: Producers avoid overproduction or shortages by aligning output with demand.

Table: The Role of Market Equilibrium in Different Sectors

| Sector | Impact of Market Equilibrium | Example |

|---|---|---|

| Housing Market | Balances housing supply and demand, stabilizing property prices. | Urban real estate adjustments during interest rate changes. |

| Labor Market | Aligns job supply with employer demand, reducing unemployment volatility. | Wage adjustments after inflation spikes. |

| Agriculture | Prevents overproduction by reflecting seasonal demand shifts. | Grain pricing based on harvest cycles. |

| Technology Market | Determines fair pricing as innovation affects production costs. | Smartphone pricing post-launch equilibrium. |

By understanding how market equilibrium functions across industries, decision-makers can create policies and strategies that maintain long-term economic stability. Understanding equilibrium helps a Product Marketing Manager price goods effectively and maintain healthy demand.

Equilibrium in Action

At the core of comprehension about how markets work is market equilibrium. For businesses, it translates to pricing and inventory decisions that culminate in profitability. For policymakers, it facilitates interventions that uphold fair play in society. For students and analysts, it offers a window into the subtle ebbs and flows of supply and demand.

Market Regulation and Its Influence on Market Equilibrium

While market equilibrium naturally balances supply and demand, governments often intervene through market regulation to promote fairness and protect consumers. Regulations can either stabilize or distort equilibrium depending on how they’re applied.

For example, in the housing market, rent control aims to keep housing affordable. However, when prices are capped below equilibrium levels, landlords may reduce supply, creating shortages. Similarly, in agriculture, price floors can lead to surpluses when minimum prices exceed market demand.

Key Ways Market Regulation Affects Equilibrium

-

Price Ceilings: Keeps goods affordable but can lead to shortages.

-

Price Floors: Protects producers’ income but can cause excess supply.

-

Taxation: Increases production costs, shifting the supply curve upward.

-

Subsidies: Encourages production, lowering prices for consumers.

-

Trade Policies: Tariffs and quotas alter equilibrium by limiting supply or demand.

Table: Effects of Market Regulation on Market Equilibrium

| Type of Regulation | Effect on Market Equilibrium | Example |

|---|---|---|

| Price Ceiling | Creates shortages as prices stay below equilibrium. | Rent control in urban housing markets. |

| Price Floor | Leads to surplus due to high minimum prices. | Agricultural subsidies. |

| Taxation | Reduces supply and raises equilibrium prices. | Fuel tax impacting transport costs. |

| Subsidy | Increases supply and lowers equilibrium prices. | Renewable energy incentives. |

| Trade Restriction | Limits imports, increasing domestic prices. | Import tariffs in manufacturing industries. |

Understanding how market regulation interacts with market equilibrium helps policymakers design better systems for balancing growth and social welfare. In the long term, successful regulations strive to support equilibrium without distorting natural market demand or economic efficiency.

By studying equilibrium, businesses can build a better Growth Strategy and adapt to changing market forces.

Frequently Asked Questions (FAQ) About Market Equilibrium

1. What is market equilibrium in simple terms?

Market equilibrium occurs when the quantity of goods supplied equals the quantity demanded at a specific price. At this point, the market price remains stable, meaning neither a surplus nor a shortage exists.

2. Why is market equilibrium important in the market economy?

In a market economy, equilibrium ensures that resources are allocated efficiently. It helps stabilize prices, allowing producers and consumers to make predictable decisions based on balanced market conditions.

3. What happens when the market is not in equilibrium?

When the market deviates from market equilibrium, either a surplus or a shortage occurs. A surplus means supply exceeds demand, pushing prices down. A shortage means demand outstrips supply, driving prices upward until equilibrium is restored.

4. How does market equilibrium apply to the housing market?

In the housing market, equilibrium is achieved when the number of houses buyers want to purchase equals the number of houses available at a given price. Factors like interest rates, construction costs, and population growth often disrupt this balance.

5. What factors can shift market equilibrium?

Market equilibrium can shift due to several factors, including changes in production costs, technology, consumer preferences, and market demand. External shocks — such as economic recessions or new regulations — can also cause major shifts.

6. How does market demand influence equilibrium prices?

When market demand increases, equilibrium prices tend to rise as buyers compete for limited goods. Conversely, when demand falls, equilibrium prices decrease, as sellers adjust to attract consumers.

7. What role does government play in market equilibrium?

Through market regulation, governments can influence equilibrium by setting price floors (like minimum wages) or price ceilings (like rent control). While these interventions aim to protect consumers or producers, they can sometimes distort natural equilibrium.

8. How is market equilibrium related to product marketing?

In product marketing, understanding equilibrium helps businesses set the right price point. When a product’s price aligns with consumer willingness to pay, firms can maximize profit while maintaining healthy demand — a balance rooted in equilibrium principles.

9. Can equilibrium exist in all types of markets?

Yes, equilibrium can exist in nearly every type of market — from commodities and labor to the housing market and digital goods. However, real-world conditions such as monopolies or information asymmetry often prevent perfect equilibrium.

10. What is the difference between short-term and long-term market equilibrium?

Short-term equilibrium occurs when supply and demand temporarily balance, often affected by immediate changes in production or consumer trends. Long-term equilibrium happens after all market adjustments, including capacity and market regulation effects, have taken place.